VCs review thousands of pitch decks every year and fund less than 1% of what they see. The decks that get funded are not the best-designed ones — they're the ones that answer the right questions in the right order. This guide breaks down the eight evaluation criteria that actually drive funding decisions in 2026, with the weights we've reverse-engineered from over 200 deal memos.

3:44

Median first-read time

10–15

Optimal slide count

<1%

Decks that get funded

8

Criteria that matter

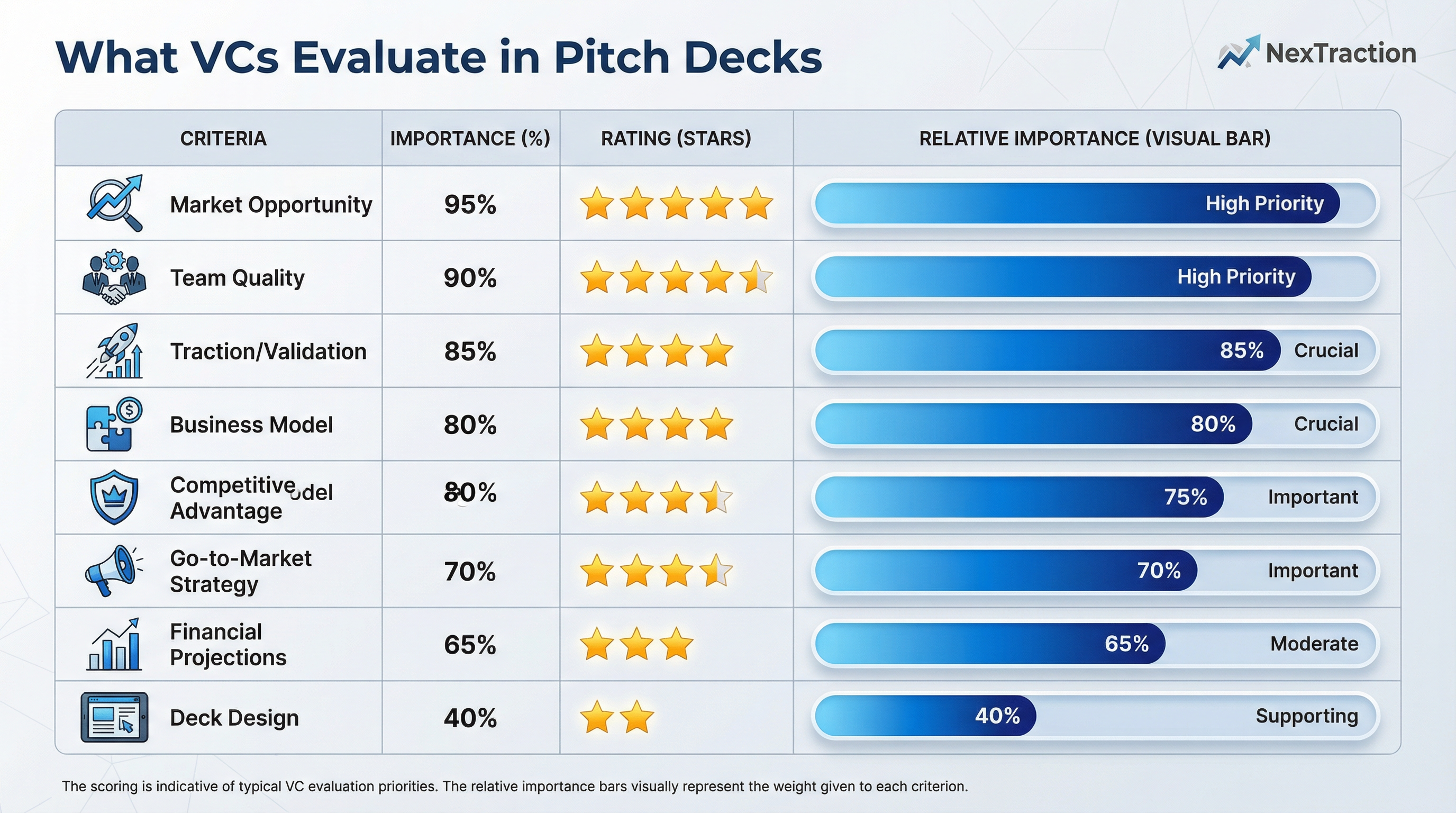

The 8 criteria, weighted

Not all slides are equal. Below is how the typical early-stage partner allocates evaluation weight when reading your deck for the first time.

| Criterion | Weight | What they're really testing |

|---|---|---|

| Market opportunity | 95% | Is the prize big enough to be venture-fundable? |

| Team quality | 90% | Why this team for this problem, now? |

| Traction | 85% | Real numbers beat any narrative |

| Business model | 80% | Can the unit economics ever work? |

| Competitive advantage | 75% | What's defensible in 2 years? |

| GTM strategy | 70% | Distribution edge, not feature edge |

| Financials | 65% | Sanity-check, not certainty |

| Design | 40% | Don't actively distract |

"I will fund an ugly deck with great numbers before I'll fund a beautiful deck with vague claims. Every time."

1 · Market opportunity

The single most important slide. VCs need to believe the addressable market can support a billion-dollar outcome. The mistake most founders make is leading with top-down logic ("if we get just 1% of a $50B market…"). Bottom-up TAM is the only way to win this slide.

What good looks like: "There are 240,000 mid-market HR teams in North America. Average willingness-to-pay is $400/month. That's a $1.15B serviceable market we can address from day one."

2 · Team quality

Investors are pattern-matching for two things: founder–market fit (do you have an unfair edge in this specific space?) and founder–founder fit (have you survived something hard together?). One paragraph per founder is enough — but each paragraph must answer: why you, why this, why now?

3 · Traction

The only criterion you can't fake. Even at pre-seed, partners look for some proof of pull: a waiting list, signed LOIs, MoM growth on a tiny base, or a sharp retention curve. Don't show vanity metrics. Show one number that matters and explain how it's compounding.

Pro tip: Stress-test every number on this slide before pitching. If you can't immediately answer "what would happen if I doubled this?", investors will know.

4 · Business model

This slide is a sanity check. VCs aren't looking for perfect unit economics at pre-seed — they're looking for awareness. Can you articulate gross margin, payback period, and a credible path to LTV/CAC ≥3x? If yes, you pass.

5 · Competitive advantage

Skip the "feature comparison matrix" — every founder has one and they all favor the founder. Instead, name your moat: distribution wedge, data flywheel, regulatory edge, or proprietary tech. One sharp moat beats five weak ones.

6 · GTM strategy

The most underrated slide. VCs have seen great products fail because the GTM was wrong. Show the distribution channel you already have a wedge into — not the channel you'll "explore."

7 · Financials

For pre-seed and seed, this is a one-slide projection: 24-month spend, headcount plan, and the milestone the round funds. Don't show 5-year revenue projections. Nobody believes them and they signal naïveté.

8 · Design

Design only matters when it's actively bad. Use one font. Use your brand colors. Don't put 12 things on a slide. The deck should feel readable in 4 minutes, which is roughly how long the partner has before they're back on Slack.

The 12-slide structure that performs

- Title — company, one-line tagline, your name

- Problem — concrete, painful, frequent

- Solution — your wedge, not your roadmap

- Why now — the timing trigger

- Market size — bottom-up TAM

- Product — one screenshot, one outcome

- Traction — the number that compounds

- Business model — pricing + unit economics

- Competition — your moat, not a matrix

- Team — why you, why this, why now

- Ask — round size, milestones, runway

- Closing — vision in one sentence

Stress-test your deck

Run your slides past four investor personas before the real meeting.

NexTraction's Virtual VC simulates the questions a skeptical generalist, a sector specialist, and a B2B-focused partner would ask. Founders who run 8+ simulated pitches stop getting surprised in real meetings.

Try a simulated pitch session →FAQ

How long should a pitch deck be?

10–15 slides for the email version. 12 slides is the sweet spot. Add a 5-slide appendix for technical or pricing detail you only show if asked.

Should I send the deck before the call?

For cold outreach: yes — it's the cost of entry. For warm intros: ask the introducer's preference. Most partners want to read first.

Do VCs really only spend 3 minutes on a deck?

On the first read, yes. The 3:44 number comes from DocSend's analysis of 200+ decks. They go deeper only if the first 3 slides earn it. That's why slide order matters more than slide design.

Conclusion

A great pitch deck doesn't get you funded — it earns you the next meeting. Optimize for that next meeting. Lead with traction, anchor every claim with a number, and make the partner feel smart for finding you. Stress-test your deck against simulated investors before it lands in any real inbox.