Due diligence in 2026 looks nothing like it did in 2018. Top deals close in days, not weeks. Founders expect investors to know their company before the second meeting. The investors who win are the ones who built a fast, repeatable DD process — without skipping the categories that actually matter. This is the complete 2026 checklist, weighted by what moves a deal memo.

6

Categories scored

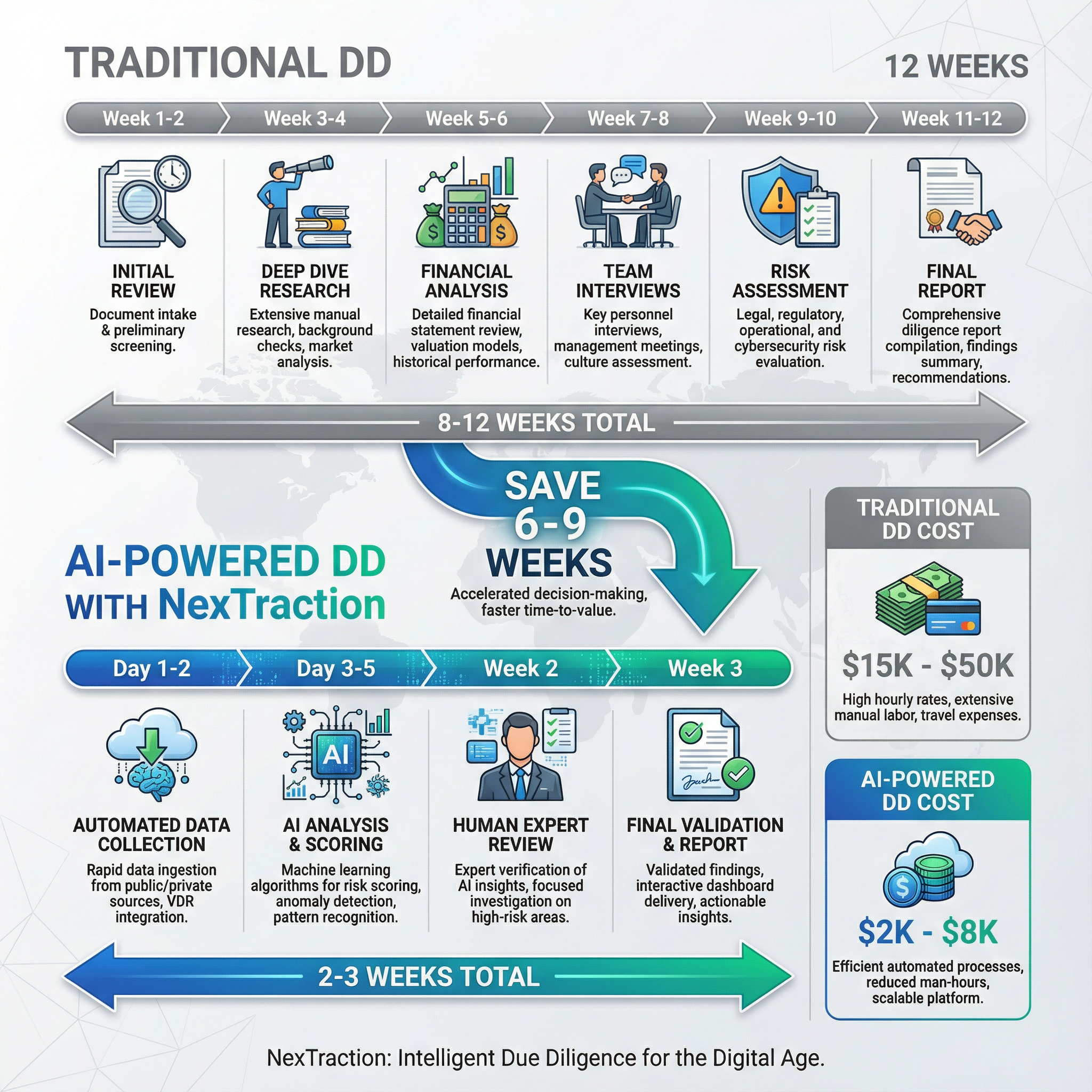

2–3 wks

Modern DD timeline

$2K–8K

Modern DD cost

5×

More deals reviewed / partner

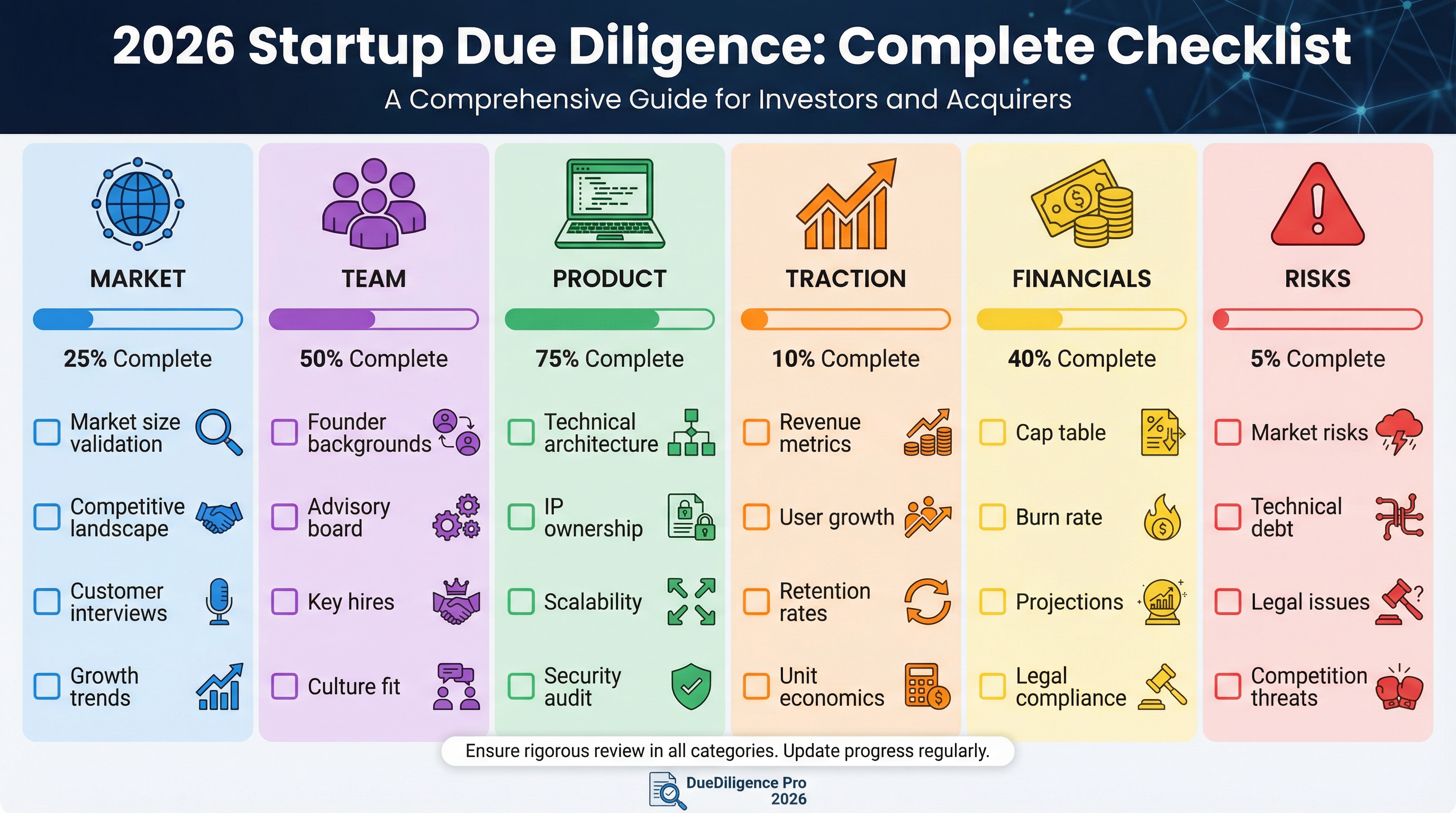

The 6 weighted categories

| Category | Weight | Key questions |

|---|---|---|

| Team | 30% | Founder–market fit · prior shipped work · team chemistry |

| Market | 25% | Bottom-up TAM · timing · displacement risk |

| Product | 20% | Wedge sharpness · roadmap discipline · technical defensibility |

| Traction | 15% | Real growth · retention curve · LOI quality |

| Financials | 5% | Burn · runway · unit economics sanity |

| Risks | 5% | Legal · regulatory · cap-table · key-person · data residency |

1 · Team (30%) — the heaviest pillar

The single biggest predictor of pre-seed/seed outcome. You're not scoring credentials — you're scoring founder–market fit (why are these founders uniquely positioned?), velocity (how much did they ship in the last 6 weeks?), and chemistry (have they survived something hard together?).

2 · Market (25%)

Bottom-up TAM only. If the founder leads with "we're going after the $2T market", penalize automatically. Look for serviceable obtainable market in the $100M–$500M+ range with credible bottom-up logic.

3 · Product (20%)

Score the wedge: one job done extremely well versus broad surface area. Score roadmap discipline: do the next 6 months focus or scatter? Score technical defensibility: data flywheel, regulatory edge, distribution wedge.

4 · Traction (15%)

The trap here is vanity metrics. Look for: cohort retention curves, real revenue (not LOIs), and what % of growth is organic versus paid. Don't pay for traction that requires increasing CAC to maintain.

5 · Financials (5%)

For pre-seed/seed, this is a sanity check, not a deep audit. 24-month burn vs runway. Honest unit economics with at least one credible path to LTV/CAC ≥3x. That's enough.

6 · Risks (5%)

The category most likely to be missed. The 2026-specific risks: data residency (where does the data live?), AI dependency (what happens if their model provider raises prices 10×?), regulatory shift (especially fintech and healthtech), key-person concentration, and cap-table cleanliness.

Traditional vs modern DD

| Traditional | Modern (AI-augmented) | |

|---|---|---|

| Timeline | 8–12 weeks | 2–3 weeks |

| Cost | $15K–50K | $2K–8K |

| Deals reviewed / partner / quarter | 10–15 | 50–80 |

| Comparability across deals | Low (bespoke) | High (structured) |

"The funds winning in 2026 aren't the smartest — they're the fastest. Founders pick the partner who came back with the sharpest deal memo in 72 hours, not the one who took 8 weeks."

The 5 silent killers most investors miss

AI vendor concentration. If 80% of their COGS is one model provider's API, that's a single point of failure. Ask the question.

Data-residency contracts. Selling into EU, UAE, or India? Check where the data physically lives. A bad answer can sink an enterprise deal.

Cap-table dilution traps. Earlier convertible notes with 10× caps that haven't converted yet can crush founder ownership at Series A.

Key-person risk. If the technical co-founder leaves tomorrow, does the company survive? Always ask the founder team this question separately.

Pricing fiction. "Customers pay us $50K/year" — is that one customer or twelve? Always normalize stated revenue against signed contracts.

For investors

Score deals on consistent axes — not investor gut.

NexTraction's investor workspace runs every deal through the same 6-category scorecard. You can compare three companies side-by-side on the metrics that actually predict outcome — and ship a deal memo in days, not weeks.

FAQ

How long does modern DD take?

2–3 weeks for a structured first-pass on a seed-stage company. Late-stage and complex transactions still need 4–6 weeks regardless of tooling. The category that compresses most is "research" — the human judgment categories don't.

What can be automated vs what can't?

Automate: market sizing, competitor mapping, traction normalization, structured scoring. Don't automate: founder reference calls, technical architecture review, customer reference quality, legal review.

Should I publish the scorecard to the founder?

Yes. Founders close faster with funds that share their reasoning. Opacity in 2026 is a competitive disadvantage.

Conclusion

Modern DD isn't about being lazy — it's about reallocating human judgment to the parts that actually need it. The funds that win in 2026 are the ones that compressed everything else. Run your next deal through the structured workspace and see what changes.